Begge lande formår at holde bolden i gang i maskinindustrien, men der er tiltagende vanskeligheder. Niveauet af langvarige betalinger er højt på begge markeder.

European football championship 2016

Sector playing field: machines/engineering

Czech Republic: the ball keeps on rolling

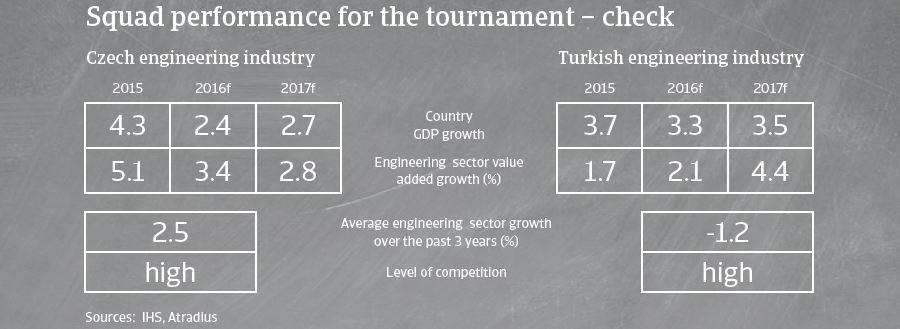

The Czech machines/engineering industry continues to benefit from the solid performance of the Czech economy, especially in the automotive industry, which is the main customer for machines. Additionally, machinery demand from the construction sector has picked up again. The very export-oriented Czech machinery industry also benefits from the recovery in the eurozone and a stable koruna euro exchange rate. The appreciation of the USD against the koruna helps machinery businesses when exporting to overseas markets. Just a few Czech machinery businesses are negatively affected by the repercussions of the Ukraine crisis.

Higher demand and a decrease in commodity prices has led to increased margins over the past twelve months. Machinery companies’ equity is above the average of all manufacturing sectors. Banks are positive about the sector in general, providing sufficient liquidity.

Turkey: mainly scoring at away games

The Turkish machinery sector faces some troubles, with sales under pressure since 2015. Political uncertainty leading to capital expenditures and high interest rates have a negative effect on the industry. In 2015 machinery exports fell 11.7%, while imports decreased by 10%. The decline in the export sector was largely due to demand from Russia, Iraq and Azerbaijan.

The decrease in commodity prices like metals helped to sustain business profit margins, but competition in the Turkish machinery market is high due to some overcapacities leading to price wars. At the same time Chinese competitors are improving their productivity, catching up in terms of technology and overall quality while maintaining lower costs.

Turkish machinery businesses with insufficient equity and long sales terms tend to use bank loans more, however, due to more volatile political and economic conditions and a high amount of non-performing loans banks have become more restricted.

Players to watch

Czech Republic

The Czech manufacturing industry is developing very well, and therefore the outlook for manufacturing machines is positive.

The agriculture machines subsector benefits from increasing demand and better financial results of customers in the agro-business segment.

Machinery businesses depending on exports to Russia or the energy sector as customers continue to face difficulties.

Turkey

In 2016 it is expected that positive developments in the construction and automotive sectors will support demand for machines.

Due to external demand-driven weakness in the textile and garment industry, machinery sales related to this industry are projected to lose volume.

In 2015, machinery exports to Russia contracted 45% year-on-year. Turkish machinery exporters dependent on this market may have trouble compensating for lost market share elsewhere. The same accounts for machinery exporters to Iraq and Azerbaijan due to the political and economic problems in these countries.

Major strengths and weaknesses

Czech machinery/engineering industry: strengths

Turkish machinery/engineering industry: strengths

- Good order situation from domestic and export markets

- Good access to financing as banks are willing to lend

- Low default rate

- Exposure in advanced markets

- Decreased raw material prices (steel and metals)

- Low labour costs compared to developed markets

- Skilled and experienced staff

- Expected to benefit from the economic rebound in Italy

Czech machinery/engineering industry: weaknesses

Turkish machinery/engineering industry: weaknesses

- Dependence on the economic cycle

- Longer cash cycle

- Highly competitive environment, with smaller machinery companies forced to compete on prices and payment terms

- Concentration of risk in larger projects

- Large investments in production facilities required

- A difficult economic and political environment limits machinery investments

- Restricted bank lending

- Not enough investment in research and development

- High funding costs for machinery investments

- Insufficient state incentives and subsidies

- Rising competition from Asia

Fair play ranking: payment behaviour and insolvencies

Czech machinery/engineering industry

On average, payments in the Czech machinery/engineering sector take between 30 days and 60 days, depending on the segment. Sometimes prepayments are needed if special tools are manufactured.

The level of protracted payments is high, often due to disputes, long inventory of accounts receivables or project delays.

Non-payment notifications are not expected to increase in the coming months.

The number of insolvencies in the industry is average compared to other industries, and no major increase is expected in the second half of 2016.

Turkish machinery/engineering industry

Payment duration in the machines/engineering sector is between 90 days and 120 days on average.

The level of protracted payments is high.

Machinery insolvencies have increased over the past six months, and are expected to level off in the coming six months. However, more insolvencies are expected if the currently difficult economic and political situations should deteriorate further.

We have scored the credit risk situation/business performance outlook for the machinery/engineering industry in the Czech Republic and Turkey. Now it's your turn to submit a score for the football match on June 21. Join the Atradius Football Championship here.