Having drawn from the expertise of Atradius Collections' local offices, the International Debt Collections Handbook explains the different regulations and procedures for debt collections in Ireland.

Amicable collections

General information

Atradius Collections’ collectors initially try to collect debts by a cycle of telephone calls and letters without recourse to legal action. We always try to obtain payment of the debts in full, but if required, we will negotiate to agree on a payment plan or a settlement figure. In the event that we consider it necessary to escalate beyond amicable collections, we must support this process in Ireland by the issue of a Letter Before Action (LBA), which is the start of the legal proceedings. This is not used in all cases, only those where our collectors consider that the debtor has the ability to pay and needs some strong evidence of our intentions. If there is no positive response to the Letter Before Action and we consider it cost-effective to do so, we will recommend that we issue proceedings in the local court. This has to be done in Ireland by one of our legal partners, although Atradius Collections will continue to be the point of contact for our client. It is necessary in Ireland for the solicitor to issue an Affidavit of Debt to be completed by the claimant and returned on headed paper.

Once the proceedings are issued, the court will decide whether to uphold the claim, and in doing so, we are able to apply for a judgment against the debtor. This judgment is published in the StubbsGazette to make the judgment public for those who wish to view it. Once the judgment has been awarded, the case will pass to the enforcement officer to pursue. It is worth noting that the court process in Ireland, and particularly the enforcement, is not a speedy process and can be costly. We will advise on a case-by-case basis about whether we consider it cost-effective to pursue this course of action. Tracing debtors in Ireland can also present problems due to the lack of availability of census-type information. When there is a dispute, we aim to reach an amicable solution between the creditor and the debtor. We do this by analysing all contractual documents (e.g. signed contracts, orders, confirmations, invoices and delivery notes, as well as standard terms previously agreed upon).

Interest

Late Payments in Commercial Transactions Regulations 2012

The purpose of these regulations is to give a legal effect to Directive 2011/7/EC of the European Parliament and of the Council of 16th February 2011 on combating late payment in commercial transactions. That directive repeals, with effect from 16th March 2013, an earlier directive from 2000 (Directive 2000/35/EC) on combating late payment in commercial transactions in European Communities.

Applicable interest rate

The regulations, which apply equally to public and private sectors, provide an entitlement to interest if payment for commercial transactions is late.

The regulations provide that, unless otherwise specified in an agreed contract, the interest rate will be the European Central Bank (ECB)’s main refinancing rate (as at 1st January and 1st July in each year) plus 8%.

The ECB rates in force on 1st January and 1st July apply for the following six months in each year. Only one rate will apply to a late payment – that is the rate in force on the payment date.

The ECB rates can be checked on the Central Bank and Financial Services Authority of Ireland website at www.centralbank.ie

The main provisions of the revised legislation are:

- Public authorities must pay for the goods and services that they procure within 30 days or, in very exceptional circumstances, within 60 days

- Enterprises should pay their invoices within 60 days, unless they expressly agree otherwise and if it is not grossly unfair to the creditor

- Enterprises are automatically entitled, without the necessity of a reminder, to interest on late payments plus compensation costs

- The statutory interest rate for late payment is increased

- Enterprises can challenge grossly unfair terms and practices.

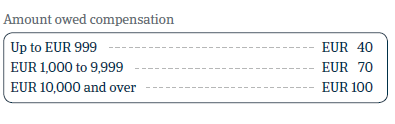

Debt collection costs

As well as interest, the supplier may also charge an amount to compensate for the costs of collecting late payments. The amount of compensation that can be claimed is determined by the outstanding amount as follows:

The Debt Collections Handbook presents a snapshot of Ireland's economic situation and covers the following topics:

- Accepted and most common payment methods

- Types of companies

- Legal procedures

- Enforcement in debt, movable and immovable property

- Insolvency proceedings

To read more about steps and procedures undertaken in debt collections in Ireland and other countries: