Long payment periods put pressure on smaller suppliers

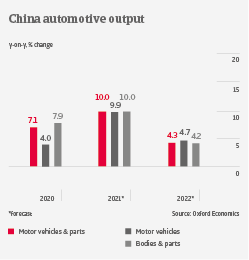

Chinese automotive output is forecast to increase 10% in 2021 and by about 4% in 2022. After a 6.5% decrease last year, car sales are expected to grow about 6% in 2021, and 7.5% in 2022. Due to higher production and sales, profit margins of many automotive businesses rebounded in H1 of 2021.

However, Original Equipment Manufacturers (OEMs) have had to reduce production due to semiconductor shortages. This affects deliveries of Tier 2 & 3 suppliers, leading to slower cash collection. Should the chip shortage last in 2022, businesses in this segment could face increasing payment delays and defaults, as many of them show lower margins and tighter liquidity compared to OEMs and Tier 1 companies.

The electric vehicles segment is a promising market in the long-term. However, the government has announced to gradually phase-out subsidies for e-mobility. A consolidation process is ongoing, and we expect that more low-cost suppliers that produce basic parts and have widely benefited from subsidies in the past will leave the market. Only those businesses with access to external funding and the ability invest in R&D constantly will survive.

With 90 - 120 days on average, the overall payment period in the industry is quite long. Larger car producers tend to pay suppliers slowly, usually with longer payment terms and bank drafts. This adds additional pressure to the margins and the capital base of smaller and/or private-owned suppliers.

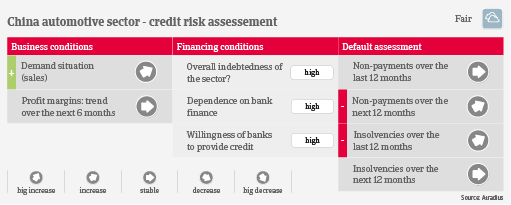

Due to their financial strength, our underwriting stance remains generally open for OEMs and Tier 1 suppliers. However, we are more cautious with Tier 2 & 3 suppliers, as lower production due to semiconductor shortage and a long payment cycle squeeze the margins and liquidity of smaller businesses. Small car dealers have recorded slim margins due to discount rates needed to stimulate sales after the slump in 2020. Fierce competition and the tight liquidity situation of the mostly private-owned businesses in this segment remain issues.