Ungarns økonomiske vækst forventes at stige i 2017 og 2018, men en meget høj udlandsgæld kan på sigt blive et stort problem for de ungarske virksomheder.

Political situation

Head of state: President Janos Ader (since May 2012)

Head of government: Prime Minister Viktor Orbán (since May 2010)

Population: 9.7 million

Troublesome relationship with the EU remains

The ruling conservative coalition of the Fidesz and KDNP parties under Prime Minister Viktor Orbán has repeatedly taken actions that led to confrontations with the EU commission and its EU peers (e.g. a controversial media law, some constitutional amendments curbing judicial independence, and a tough stance in the migrant policy, together with a lack of willingness to accept the mandatory quotas for refugees passed by the EU). Together with some unorthodox economic policy decisions like additional taxes on banks, the government’s repeated confrontations with the EU have led to some uncertainty among its European peers and international investors.

Economic situation

Slower growth in 2016, followed by a rebound in 2017

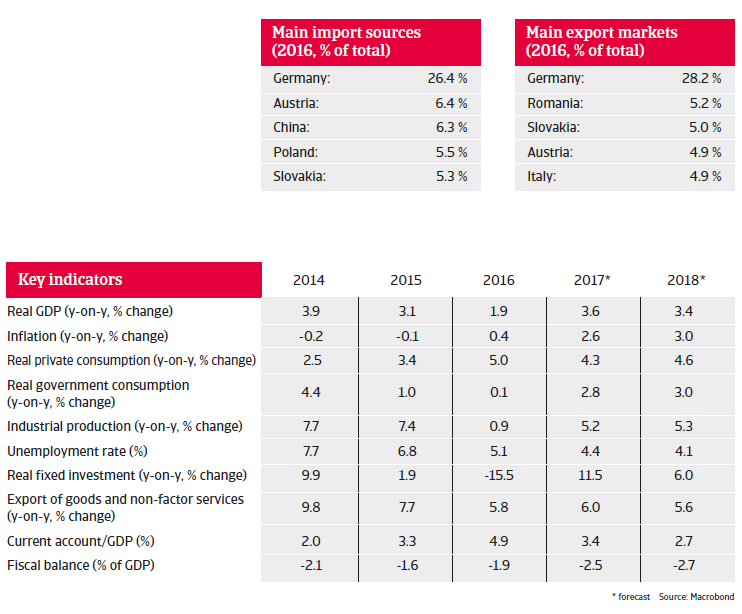

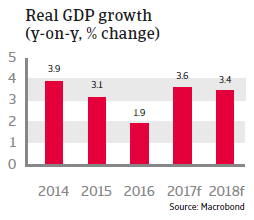

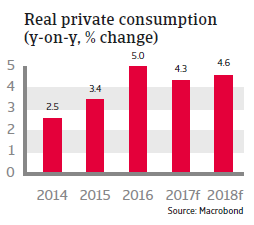

Hungary´s GDP growth slowed down to 1.9% in 2016, as public spending on infrastructure sharply decreased (lower disbursement of EU funds). That said, economic growth was sustained by robust private consumption (up 5.0%).

In 2017 and 2018 economic growth is forecast to increase by about 3.5% annually as private and public investments have picked up again. After deflation in 2014 and 2015 (mainly due to regulated household energy prices) consumer prices have started to grow again, and are forecast to increase 2.6% in 2017 and 3.0% in 2018.

Private consumption growth will be driven by wage growth (minimum wage increases in 2017 and 2018) and increasing employment, while exports (driven by eurozone demand) are expected to remain solid. Risks stem from an end of the eurozone rebound and a cooling down of world trade, which would hurt Hungarian export growth.

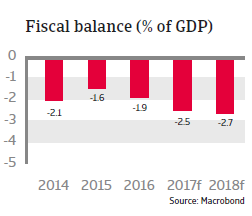

Containing the budget deficit within 3% of GDP is a top priority of the administration in order to avoid EU sanctions. However, since 2010 the government has been using unorthodox ways to balance the budget, most notably extraordinary taxes on banks and utilities. The budget deficit is forecast to increase in 2017 and 2018 due to lowered corporate taxes and social security contributions and VAT decreases. Public debt remains high at 77% of GDP (Central-Eastern Europe median is 52% of GDP), but fiscal consolidation policies will be postponed until after the general elections in 2018.

High debt level is a major weakness

Hungary’s major weakness remains its high level of external debt (almost 100% of GDP in 2017). A large share of it is foreign currency-denominated, which exacerbates the problem, as a forint depreciation would hurt many Hungarian households and businesses whose loans are denominated in foreign currencies. Additionally, more than 30% of public debt is denominated in foreign currency.

Despite the fact that current account surpluses bolster the exchange rate, the forint remains highly vulnerable to international investors’ sentiment due to the high external and public debt levels and a suboptimal institutional and policy environment.