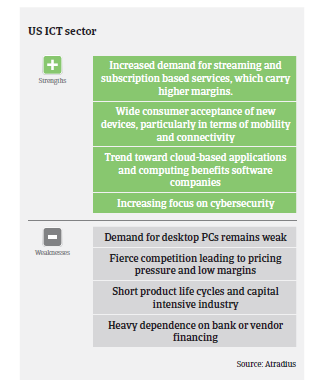

Despite healthy growth in many ICT segments, stiff competition is leading to low pricing and margin compression for distributors and retailers alike.

- Full impact of Sino-US trade dispute still remains to be seen

- Insolvencies not expected to decrease in 2018

- Payments commonly range between 30 and 90 days

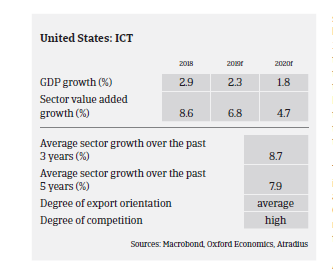

In 2018, the US ICT market benefitted from robust economic growth and a further increase in private consumption, aided once again by wage growth and employment gains. This positive trend should continue in the coming months.

According to the Consumer Technology Association (CTA), retail revenues in the US consumer technology industry grew 6% year-on-year in 2018, reaching a record-breaking USD 377 billion. Another 5.5% increase is expected in 2019.

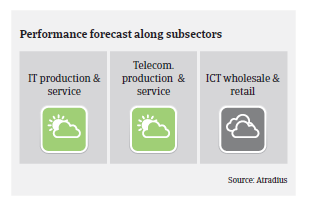

2019 growth in the smartphone segment should slow somewhat, with revenues forecast to increase 2% and unit volumes up 1%. That said, the planned introduction of 5G smartphones will drive demand moving forward. Smart speakers, smart home, smartwatches and drones are expected to see revenue growth of 7%, 17%, 19% and 4% respectively.

With a 25% year-on-year increase, streaming services recorded the highest annual growth rate in 2018. The US remains the world’s largest market for media content, access and technology, but with increased concentration on subscription services and less on the single-unit purchases that drove consumer spending for decades.

Despite the healthy growth rates in many ICT segments, stiff competition is still leading to low pricing strategies and margin compression for distributors and retailers alike. Any margin gains are likely to come from new product lines or a greater portion of sales being derived from services, which tend to carry higher margins. Margins of ICT manufacturers are impacted by the already high market penetration of mature product categories and the subsequent need for innovation, which leads to higher R&D costs.

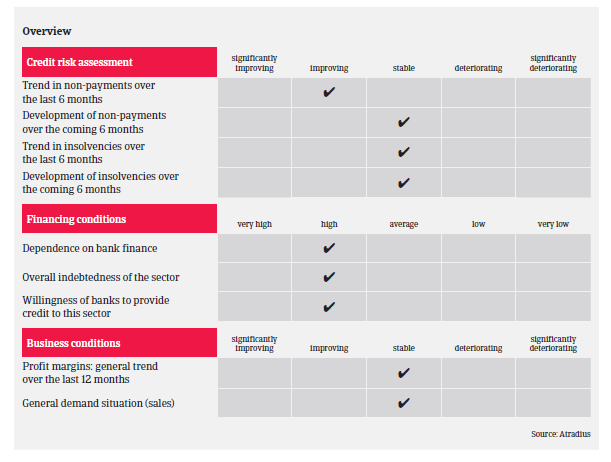

Payment behavior in the US ICT sector has improved slightly over the past 12 months. Payments in the industry commonly range between 30 and 90 days, but in some cases can take 120 days. When payment delays occur, they generally relate to disputes over product pricing or other issues, as opposed to liquidity concerns. Manufacturers often offer price protection or discounts on products in order to move inventory ahead of the rapid innovation of technology experienced in the market. This can lead to disputes and ultimately an increase in non-payments until the issues can be resolved.

There was no major ICT insolvency in 2018, and business failures are expected to level off in 2019. A substatinial decrease cannot be expected, given the ongoing high level of competition, the abundance of start-ups and the ever short product cycles.

Currently the full impact of the ongoing escalation in the US-China trade dispute still remains to be seen. ICT related goods are still largely excluded from the Chinese imports worth USD 200 billion on which the US administation recently raised tariffs from 10% to 25%. For most of the affected US businesses the short-term impact of restrictions on doing business with Huawei seem to be limited (Washington added Huawei to a list of companies that US firms cannot trade with unless they have a government licence). It is expected that the main US suppliers of semiconductors, chips, and processors to Huawei are able to divert sales for the time being, thereby offsetting sales decreases to Huawei in the short-term at least.

That said, any steps to impose tariffs on essentially all remaining imports from China (valued at approximately USD 300 billion), and retaliatory measures by China would definitely affect ICT. Out of concerns over such a move many ICT companies have already started to stockpile inventory or to import required goods from other Asian markets.

A full-scale trade war between the US and China would definitely lead to higher prices for a range of consumer electronics and ICT components. It is expected that US ICT retailers could absorb some of the costs to a certain degree and partly pass on price increases to consumers, but this would have certain limits due to the very competitive market situation. Therefore, decreasing margins for retailers cannot be ruled out in such a scenario.

Some ICT companies are able to shift production from China to other countries, cutting the final bill for US consumers. Companies with complex supply chains, mainly those in high tech industries, are able to change the way their internal costs are charged to subsidiaries to lower their tariff bill. However, ICT supply chains would be hurt if there is a full-scale trade war, as ICT products assembled in China and exported to the US heavily depend on the input of US-made components (semiconductors, software and other items). Therefore, there is also a potential negative impact mainly on the component supply side.

Despite the uncertainty surrounding tariffs, our underlying underwriting strategy remains cautiously open for the time being, with a focus on favourable subsectors such as smartphones, health technology products, streaming or subscription services and other emerging technologies, mainly smart or connected devices, while being more cautious with declining subsectors like PCs and semiconductors.

Relaterede dokumenter

1.13MB PDF